By Charles Huang

For eighty years, the US dollar has been the anchor of global finance – the currency of oil deals, central bank reserves, and international debt. Yet, in 2025, that anchor started to drag. The dollar’s value tumbled against major currencies, while the Euro and Yen surged and central banks stockpiled gold and silver as hedges. The world isn’t abandoning the dollar overnight, but it is clearly preparing for a life not centered around it.

To understand why this moment matters, it’s worth looking back at how the dollar gained such dominance in the first place and why that dominance has lasted for nearly a century. After World War II, the 1944 Bretton Woods Agreement established the dollar as the world’s reserve currency, backed by gold and supported by America’s unmatched industrial strength. When the gold standard was abandoned in 1971, confidence in US institutions and markets kept the dollar at the heart of global finance. The petrodollar system, where oil is priced and traded exclusively in dollars, further reinforced the dollar’s reach. Over time, US Treasury securities became the bedrock of global investment portfolios. Even during crises like the Asian financial collapse, 2008 recession and pandemic turmoil, investors have sought shelter in the dollar. That legacy explains why this year’s consistent decline feels so consequential. The same foundations that once made the dollar untouchable– trust, liquidity, and global reach– are now being tested in real time.

Now, the effects of that test are playing out in markets around the world. In the first half of 2025, the US Dollar Index dropped roughly 10%, its steepest fall in over fifty years, as concerns over US debt, widening deficits, and slower growth rattled investor confidence. The International Monetary Fund (IMF) reported that the dollar’s share of global reserves slipped to around 57.7% in early 2025, underscoring how central banks and other institutions are diversifying their holdings. The euro and yen have both gained ground, and countries like India and Brazil have shifted away from US treasuries into gold, silver, and other more stable assets. The dollar’s weakening reveals how dependent its strength has become on the perception of US credibility rather than inherent fundamentals. As that credibility frays under record deficits and political gridlock, the dollar’s “safe-haven” status begins to look less like a guarantee and more like a gamble. Ultimately, the question becomes whether the US dollar still deserves the trust that gives it its inherent value.

Markets are no longer pricing in American exceptionalism, and decades of deficit spending, rising national debt, and political dysfunction have begun to erode this long-standing fiscal foundation.

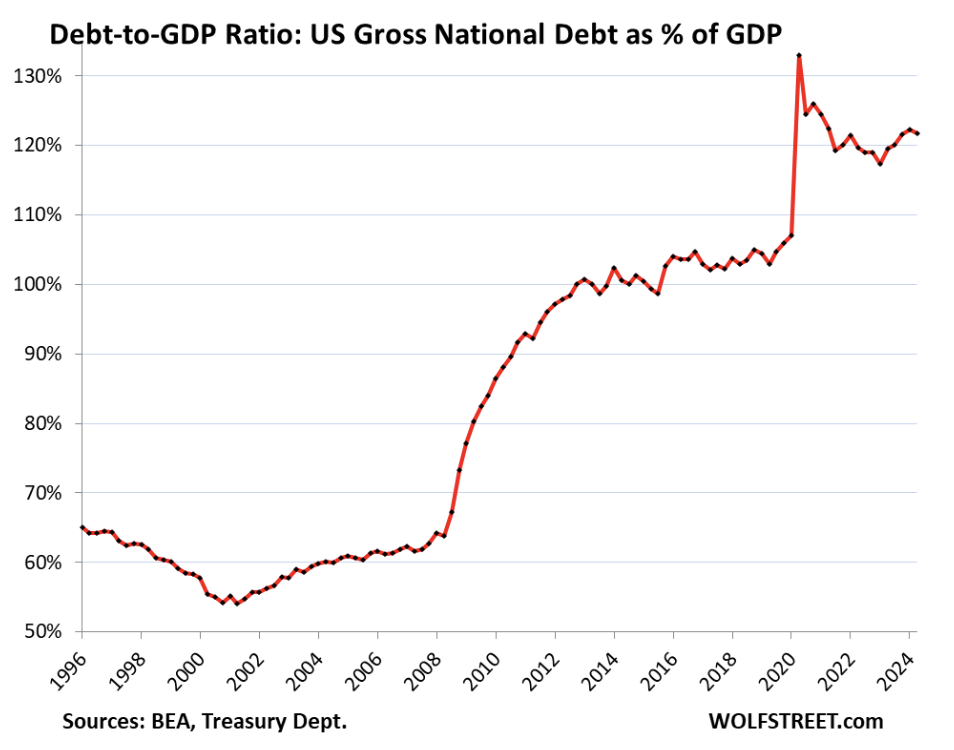

The US debt-to-GDP ratio has surged past 120%, and with interest rates now consuming a growing share of federal revenue, investors are reassessing whether the “risk-free” asset still deserves that label. As JPMorgan analysts noted, slower US growth and widening deficits have amplified fears that the US’s fiscal trajectory is unsustainable, resulting in capital outflows and weakening demand for dollar-backed assets. Foreign investors, once reliable buyers of US Treasuries, are increasingly hedging their exposure. Goldman Sachs Asset Management reports that global funds have been diversifying current risk and channeling capital toward other currencies or commodities backed by other currencies. This shift, however, also recalibrates geopolitical risk and the use of the dollar as a sanctions tool (most notably against Russia). Other nations are wary of an overreliance on a financial system governed by US policy. In short, the dollar’s weakness is not a symptom of a temporary downturn but rather a manifestation of deeper structural fatigue, and investors are now starting to recognize the vulnerability of the US dollar.

For the United States, the implications of a weaker dollar are immediate and tangible. A weaker dollar erodes the “exorbitant privilege” that has long allowed Washington to finance spending cheaply.

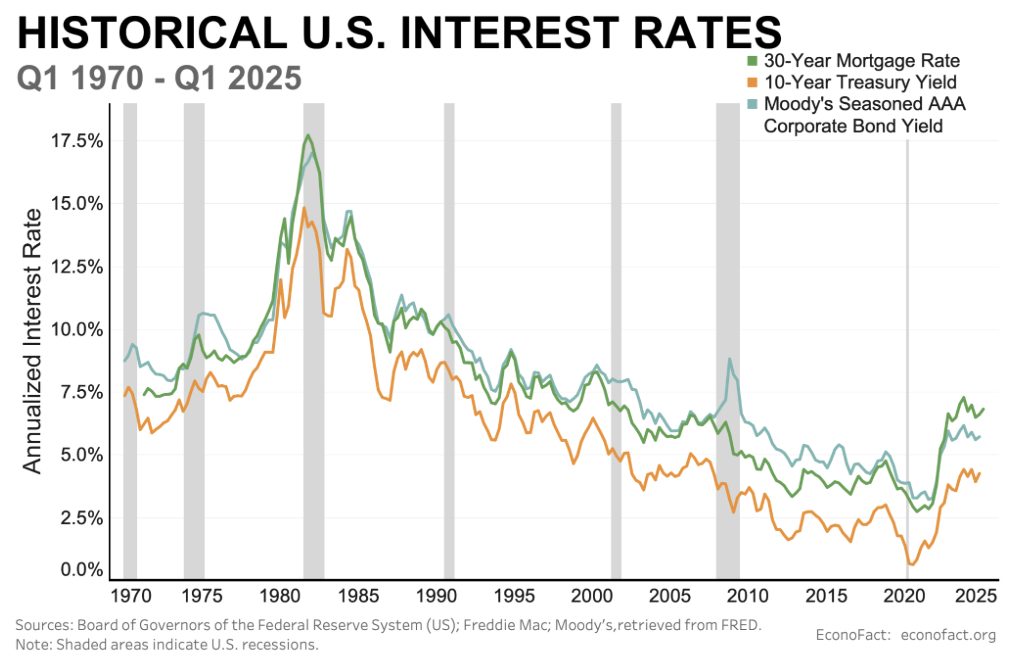

As Treasury yields climbed past 4.7% this summer, up nearly a full percentage point from last year, the cost of servicing America’s $35 trillion national debt has risen sharply. Interest payments now consume 14% of federal revenue, the highest share in decades. The government overall faces higher borrowing cost, tighter fiscal space, and mounting pressure on future budgets. Increasingly, people ranging from portfolio managers to your average citizen are hedging exposures in other safe-haven assets like short-term bonds and gold, which has climbed to a record high of over $2450/ounce this past summer. As the US’s monetary dominance is being questioned, the nations within BRICS – an intergovernmental organization composed of international powerhouses such as China, Russia, and India – have expanded the use of their local currencies in trade settlements. In the oil industry, countries like Saudi Arabia are experimenting with non-dollar oil contracts.

The dollar’s dominance may not collapse tomorrow, but the cracks in its foundation force an uncomfortable question: should the world really rely on any single national currency to be the backbone of global trade? The truth is that every transaction, from oil contracts to sovereign loans, remains priced relative to the dollar. Not because it is perfectly stable, but because nothing better exists. Even as nations diversify, the system itself orbits around the US’s fiscal gravity, and when US deficits swell or policy shifts abruptly, the whole world feels the tremor. This dependence exposes a deeper flaw in how global commerce is built upon a currency whose supply, value, and credibility are controlled by one government, for its own domestic priorities. The idea of a synthetic reserve currency, a digital composite benchmarked to a basket of major currencies and commodities, has long been theoretical; however, the current turmoil lends it new relevance. The IMF’s Special Drawing Rights (SDRs) hint at this model, yet they remain limited in scope and adoption. A truly independent global unit of account, insulated from national debt politics, could offer a fairer and more stable foundation for trade and finance. Such a shift could be radical, but so was Bretton Woods in 1944. “Ditching the dollar” isn’t about erasing it– it’s about redefining the standard so that no single economy should affect the world’s balance sheet.

At the end of the day, the dollar won’t vanish overnight. Its depth, liquidity, and political backing still make it indispensable to the global economy. But 2025 has shown us how fragile that privilege is, and the assumption that the dollar will always rebound is no longer safe. For investors and young professionals, the key takeaway is practical: hedge exposure, diversify holdings away from the US dollar, and pay attention to how global policy affects our currency. In the meantime, gold, short-term bonds, and even other major currencies such as the yen or euro may prove to be safer options. And while the idea of a universal, synthetic currency remains distant, too complex politically and early technologically, each hit to the dollar makes it seem less and less far-fetched. Someday, perhaps in our lifetimes, such a system detached from a single government’s debt may become the solution to the world’s monetary problems. For now, though, it’s not the time to truly ditch the dollar. But it is time to stop assuming that it is untouchable.