By Evan Draga and Shawn Boehmer

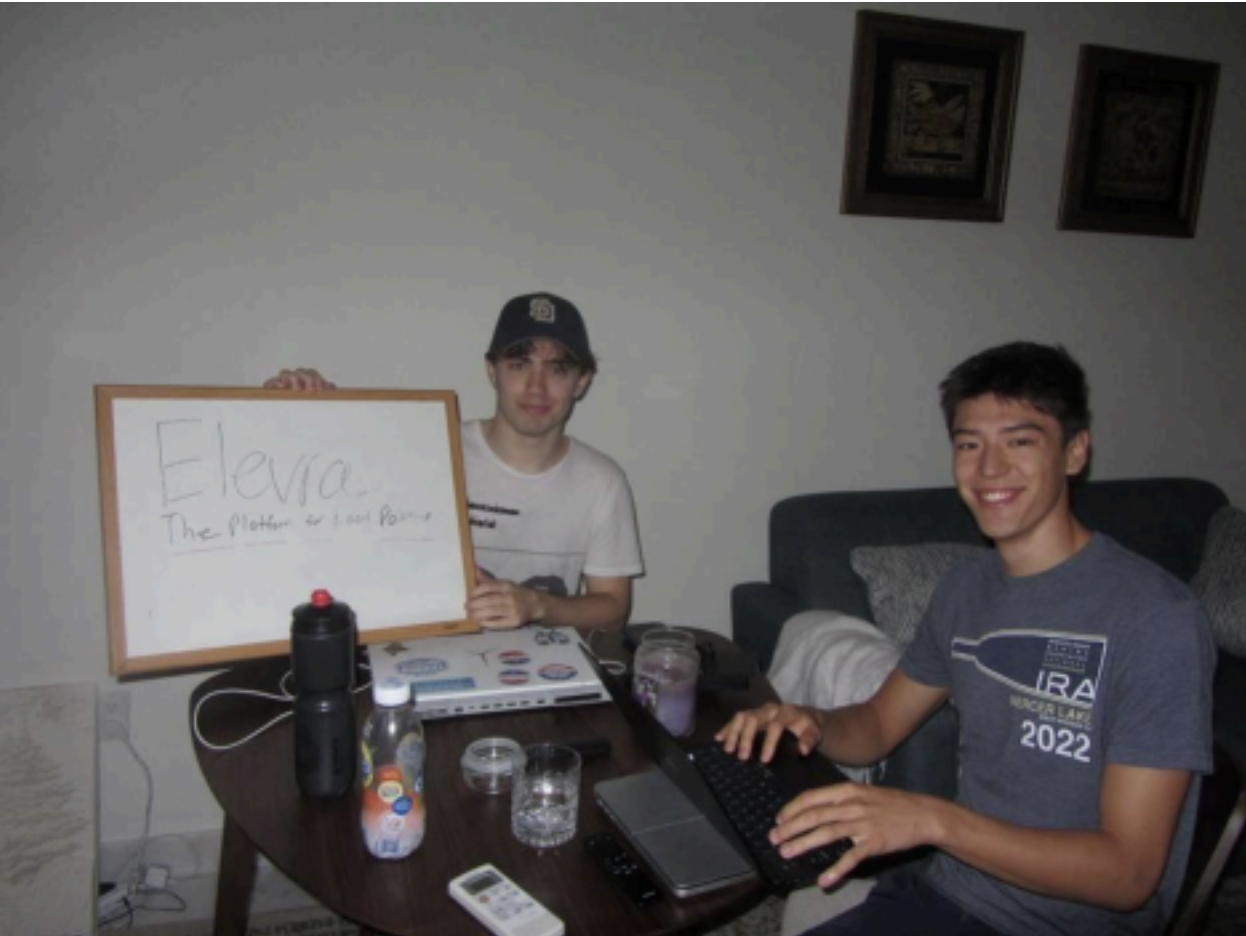

Last year, two Cornell seniors started Civoren, a startup that aims to democratize U.S. elections. The founders, Adam Rose and Sam Alston, recently left their jobs in finance to pursue the vision full-time. In an interview with Shawn Boehmer of The Harvard Crimson, Adam described a vision that goes far beyond campaign websites or easier election browsing. He wants to build the central platform for American elections: the place voters go to understand who is running and engage with campaigns, and the place candidates go to be discovered, define themselves, and run their campaigns.

By Aaron D. Friedman and Adam G. Rose

Backstage at Manhattan’s Marquee venue, Michael Natenzon, Damian Cacciato, and Michael Goldman finalize their set minutes before Blank Hospitality’s debut performance. This moment was once a distant vision for Natenzon, Cacciato, and Goldman, founders of a hospitality firm that has since expanded from the stages of New York to an international platform, hosting, organizing, and performing at events in Miami, Canada, Israel, Portugal, and the French Alps.

By Natalie Hughes

It’s without doubt that the global economy continues to reel from the effects of stay-at-home and pandemic restrictions around the world. In the U.S. alone, countless retail giants have been forced into bankruptcy, commercial real estate has been permanently impaired, and the Federal Funds Rate has plummeted. Unfortunately, those misfortunates are transpiring on an international scope as well. However, recent reports of budding Merger & Acquisition activity demonstrate some promise for potential revitalization. While certain sectors and fiscal statistics like the ones mentioned may take more time to recuperate, there remains hope for global M&A. Activity hit a record $1.3 trillion this past quarter and has shown the strongest start to the year in three decades. Not only is this figure the largest of any Q1 ever, but it’s also the second-largest of any quarter in world history. Additionally, the value of impending and completed deals jumped 93% from Q1 of 2020 while the total number of deals increased 9%.

By Alexandre Taylor

On the surface, modern loyalty programs, which are now ubiquitous in consumer markets, have changed little since their appearance in American cereal boxes a century ago. Initial loyalty programs sought to retain customers by offering incentives, whether financial or physical, alongside a purchase. This spending-fueled strategy for customer loyalty management continued well into the 2000s. But firms were approaching a roadblock, one which they may have been ignoring for a long time. Customer loyalty programs weren’t all that profitable. The reason was obvious – everyone was doing it.

by Emily Xiao

You’ve witnessed it firsthand--COVID-19, quarantine boredom, and mass digitization. Over the past year, people have stayed home with little to do, and companies have rapidly adapted their sales strategies in response. This means, of course, an increase in online shopping, much to the detriment of brick and mortar retail. And what’s more is that tech-savvy young consumers seem to dictate emerging shopping trends. Gen Z and millennials’ current fixation? Sustainability.

By Strauss Cooperstein

Employment opportunities at investment banks remain highly sought-after. But do six-figure salaries make the progressive wear on young analysts’ minds and bodies worth it? Several recent outcomes as a result of the Covid-19 pandemic and skyrocketing markets suggest they are not. Conversations regarding mental health in the workplace became increasingly contentious when a slide deck from 13 anonymous first-year Goldman Sachs employees circulated, each describing how 100-hour weeks had the ability to put them “in a really dark place” or feel “like a disposable-number cruncher” and a “punching bag.”

By Natalie Hughes

With the abundance of home lockdowns and quarantines throughout the past year, revenues of at-home delivery services have skyrocketed to unprecedented levels. This information bodes very well for companies like Deliveroo, a U.K.-based, Amazon-backed food delivery service. As a result of the firm’s recent success, the Deliveroo executive team has made the decision to go public in hopes of raising capital and expanding its business. The company is projected to raise a whopping £1 billion (the equivalent of $1.38 billion) in said Initial Public Offering next month when it begins to trade on the London Stock Market. However, as vaccines continue to roll out and more citizens begin to brave outdoor and indoor dining experiences, it’s unclear how sustainable the growth of delivery services will be.

By Raghav Madhukar

Elon Musk recently made headlines for surpassing Bill Gates’ net worth, securing the Tesla CEO’s spot as the second wealthiest person in the world. The latter’s fortune (currently valued at a whopping $ 128 Bn) rose in response to Tesla’s unwavering stock rally, which is set to finish the calendar year on a high.

By Natalie Hughes

If you’ve been involved in an organization, whether in an academic, professional, or social setting, then you’re probably familiar with business communication platforms. Salesforce and Slack are two industry giants whose software is installed within the networks of organizations across the United States. Salesforce, an American cloud-based software company, provides customer relationship management services. Slack, another business communication program that has altered the way businesses operate internally, is primarily a channel-based messaging platform. As COVID-19 continues to alter the way workplaces are functioning, demand for tools which enable remote work has risen greatly. Needless to say, systems like Slack and Salesforce have evolved into corporate necessities and are shaping the state of business in the United States.

By Strauss Cooperstein

In order to pull the “economic center of gravity back towards Asia” amid the COVID-19 pandemic, one of the most powerful free trade agreements in Asia Pacific history was drafted on November 15th at a virtual summit in Vietnam. Led by China, South Korea, and Japan, the Regional Comprehensive Economic Partnership (RCEP) joins together Australia, New Zealand, and the 10 original members of the Association of Southeast Asian Nations (ASEAN). The RCEP calls for the abolishment of tariffs on imports between signatories, less red-tape, and establishes rules for e-commerce, trade, and intellectual property.